Umbrella Liability Benchmarking: National vs New York

March 12, 2026

Over the past decade, Umbrella Liability Coverage for construction contractors has steadily climbed in both size and complexity. Benchmarking data from 2016 through 2025 shows a clear pattern: higher limits, more layered coverage structures, and widening regional differences, especially between national markets and the state of New York.

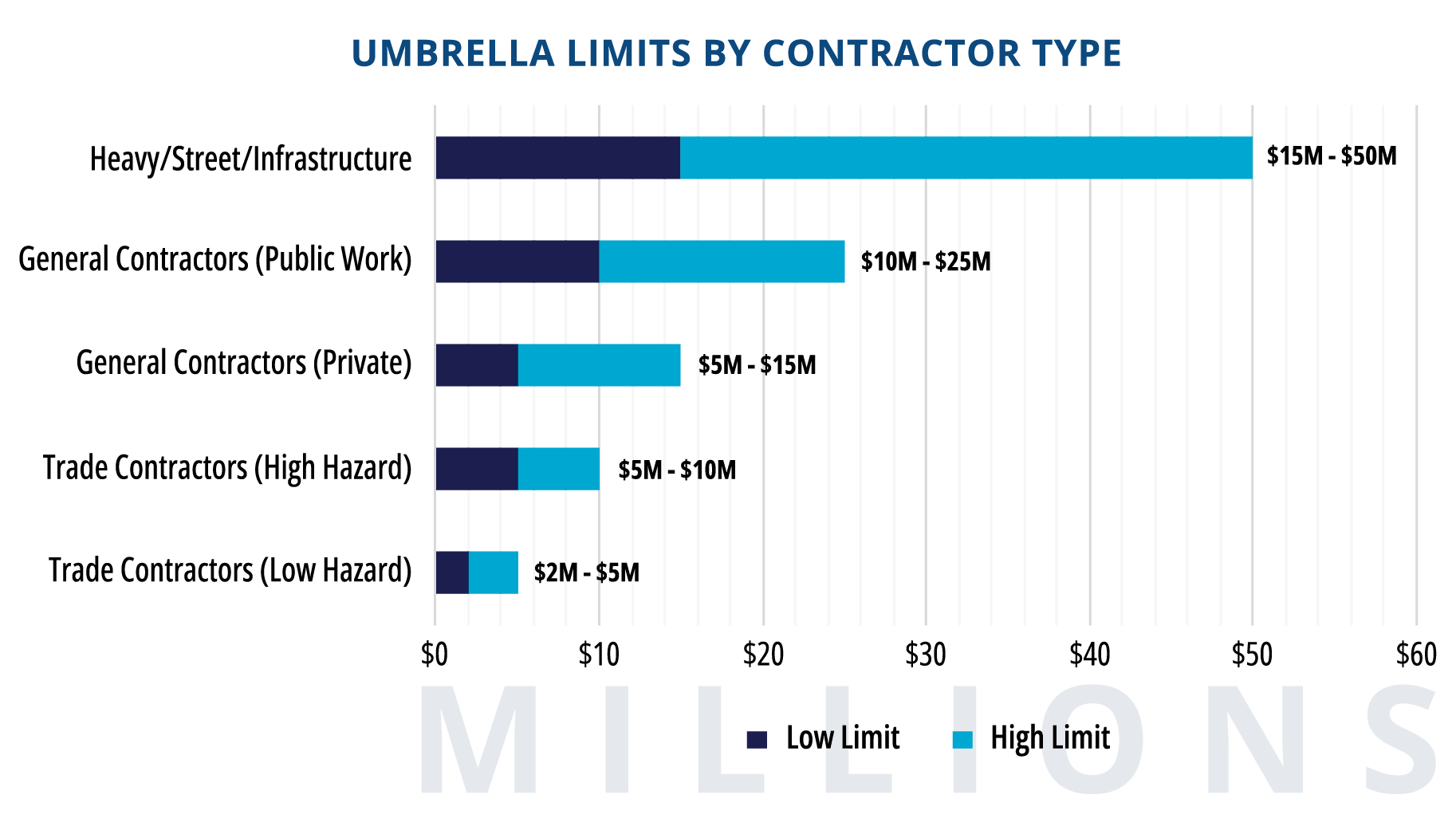

At a national level, typical Umbrella limits for construction firms in 2025 fell between $5 million and $10 million. In the state of New York, however, limits are significantly higher – often coming in at $10 million to $25 million or more, particularly for street, infrastructure, and public works projects. Heavy civil contractors may carry umbrella programs reaching $15 million to $50 million, often structured across multiple excess layers.

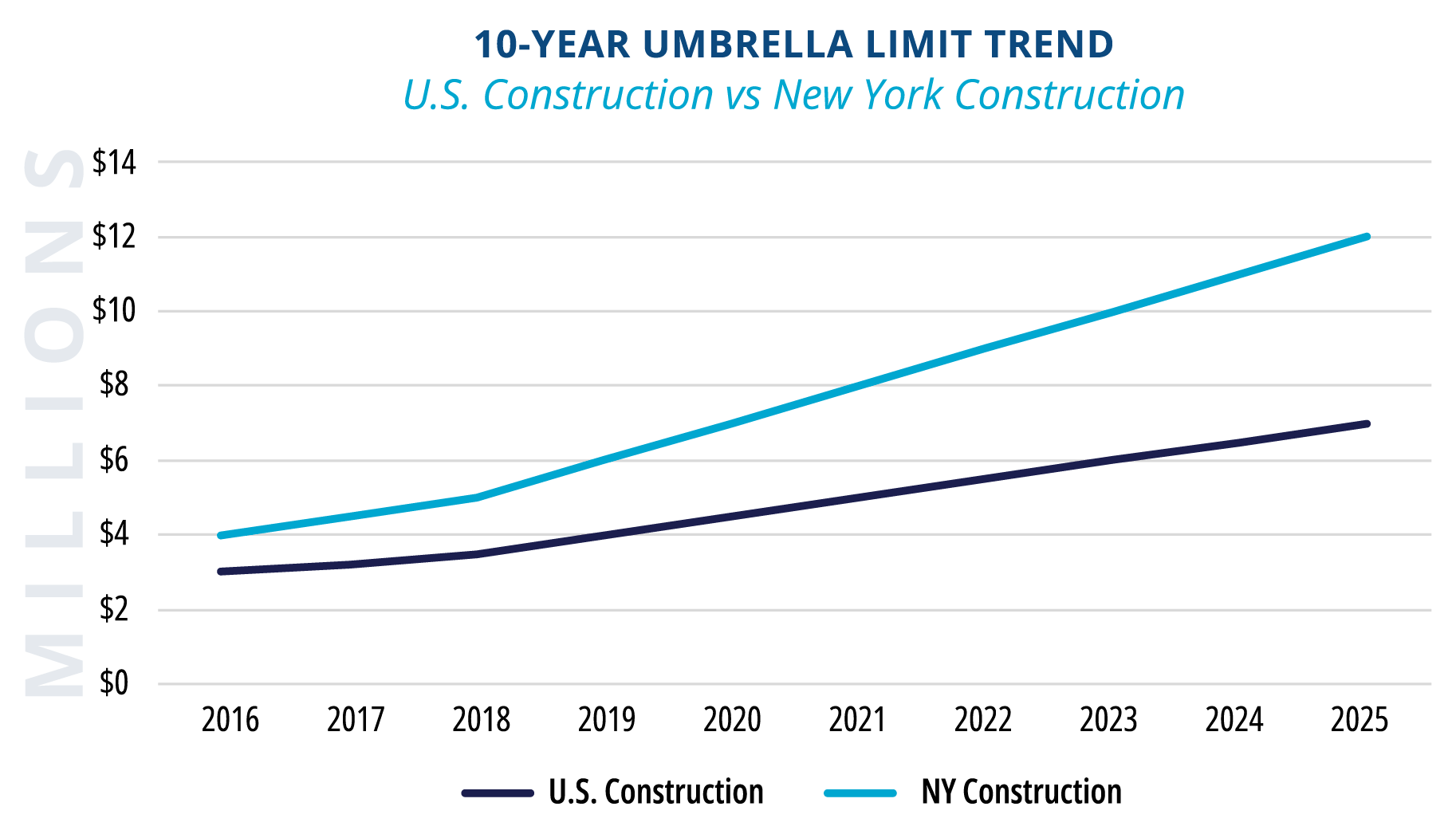

The long-term trend illustrates just how much coverage expectations have shifted. In 2016, the average Umbrella limit purchased by U.S. construction contractors was about $3 million, compared to $4 million in New York. By 2025, those averages had risen to approximately $7 million nationally and $12 million in New York. Growth accelerated after 2020, when insurers reacted to rising claim severity, larger jury verdicts, and expanding statutory liability exposures.

Coverage needs also vary significantly by contractor type. Lower-hazard trade contractors typically carry up to $5 million in Umbrella limits, while higher-risk trades often require $5 million to $10 million. Private general contractors generally fall between $5 million and $15 million in Umbrella limits, while public works general contractors frequently need up to $25 million or more to meet contractual requirements.

These differences in risk are also reflected in premium costs. Across the United States, Umbrella Liability Coverage averages roughly $3,000 to $6,000 annually per $1 million of Umbrella limit. In the state of New York, premium pricing doubles, falling between $6,000 and $12,000 per $1 million. Heavy civil or street work yields the highest premium rates, reaching up to $20,000 per $1 million of Umbrella Limit. Interestingly, lower umbrella layers often carry the highest rate per million, while higher excess layers may be priced more efficiently once the most severe exposures are buffered.

Structural changes in the insurance market further illustrate how risk has evolved in the construction space. Earlier in the decade, single carriers frequently offered large umbrella limits with relatively simple terms; today, coverage is more commonly built through layered towers—such as $5 million + $5 million + $10 million—with higher attachment points, tighter underwriting, and more exclusions.

New York’s environment magnifies these pressures. Strict liability under the state’s Labor Law, higher jury verdicts, a concentration of large public projects, and reduced insurer appetite for certain exposures all contribute to higher required limits and more restrictive underwriting.

In totality, the data paints a picture of rising umbrella limits that are not simply a market trend—they are a structural response to legal realities, economic forces, and the growing scale of construction risk. Contractors today are not just buying more insurance; they are building more sophisticated financial protection systems to keep pace with an increasingly high-stakes risk environment.

Disclaimer: Benchmarking data shown is illustrative and directional, based on industry reports, broker market intelligence, and underwriting trends. Actual pricing and limits vary by contractor profile, loss history, project mix, and insurer appetite.

'%3e%3cpath%20d='M21.0003%200.411865C9.67681%200.411865%200.412109%209.67657%200.412109%2021.0001C0.412109%2031.1913%207.82387%2039.6324%2017.6033%2041.3824C17.6033%2041.3824%2017.6508%2041.3436%2017.7251%2041.2829C17.7188%2041.2818%2017.7125%2041.2807%2017.7062%2041.2795V26.7648H12.5592V21.0001H17.7062V16.4707C17.7062%2011.3236%2021.0003%208.44128%2025.7356%208.44128C27.1768%208.44128%2028.8239%208.64716%2030.265%208.85304V14.103H27.5886C25.118%2014.103%2024.5003%2015.3383%2024.5003%2016.9854V21.0001H29.9562L29.0298%2026.7648H24.5003V41.2795C24.4374%2041.2909%2024.374%2041.3007%2024.311%2041.3115L24.3974%2041.3824C34.1768%2039.6324%2041.5886%2031.1913%2041.5886%2021.0001C41.5886%209.67657%2032.3239%200.411865%2021.0003%200.411865Z'%20fill='%23111C4E'/%3e%3cpath%20d='M24.4998%2026.7647H29.0292L29.9557%2021H24.4998V16.9853C24.4998%2015.3382%2025.1174%2014.1029%2027.588%2014.1029H30.2645V8.85293C28.8233%208.64704%2027.1762%208.44116%2025.7351%208.44116C20.9998%208.44116%2017.7057%2011.3235%2017.7057%2016.4706V21H12.5586V26.7647H17.7057V41.2794C17.7119%2041.2805%2017.7182%2041.2817%2017.7245%2041.2828C18.8506%2041.4864%2019.9766%2041.5882%2021.1027%2041.5882C22.2288%2041.5882%2023.241%2041.495%2024.3105%2041.3114C24.3734%2041.3006%2024.4369%2041.2908%2024.4998%2041.2794V26.7647Z'%20fill='white'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_1004_2093'%3e%3crect%20width='42'%20height='42'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

'%3e%3cpath%20d='M21.5003%200.421631C9.85916%200.421631%200.421875%209.85891%200.421875%2021.5001C0.421875%2033.1412%209.85916%2042.5785%2021.5003%2042.5785C33.1415%2042.5785%2042.5787%2033.1412%2042.5787%2021.5001C42.5787%209.85891%2033.1415%200.421631%2021.5003%200.421631ZM26.2365%2033.4679L19.8509%2024.1747L11.8563%2033.4679H9.79007L18.9334%2022.8397L9.79007%209.53278H16.7641L22.8107%2018.3324L30.3814%209.53278H32.4476L23.7288%2019.668L33.2111%2033.4679H26.2371H26.2365Z'%20fill='%231B1E4C'/%3e%3cpath%20d='M12.5996%2011.0879L27.2075%2031.9831H30.381L15.7737%2011.0879H12.5996Z'%20fill='%231B1E4C'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_1004_2085'%3e%3crect%20width='43'%20height='43'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

'%3e%3cpath%20d='M21.0003%200.411865C9.62992%200.411865%200.412109%209.62967%200.412109%2021.0001C0.412109%2032.3705%209.62992%2041.5883%2021.0003%2041.5883C32.3708%2041.5883%2041.5886%2032.3705%2041.5886%2021.0001C41.5886%209.62967%2032.3708%200.411865%2021.0003%200.411865ZM14.1393%2033.5349H8.96309V16.8218H14.1393V33.5349ZM11.5263%2014.6332C9.83523%2014.6332%208.46497%2013.2521%208.46497%2011.549C8.46497%209.84585%209.83523%208.46472%2011.5263%208.46472C13.2174%208.46472%2014.5865%209.84585%2014.5865%2011.549C14.5865%2013.2521%2013.2174%2014.6332%2011.5263%2014.6332ZM33.5351%2033.5349H28.3841V24.7615C28.3841%2022.3561%2027.4702%2021.0115%2025.5664%2021.0115C23.495%2021.0115%2022.4129%2022.4104%2022.4129%2024.7615V33.5349H17.4489V16.8218H22.4129V19.0734C22.4129%2019.0734%2023.9056%2016.3117%2027.4525%2016.3117C30.9994%2016.3117%2033.5357%2018.4763%2033.5357%2022.9537V33.5355L33.5351%2033.5349Z'%20fill='%231B1E4C'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_1004_2088'%3e%3crect%20width='42'%20height='42'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)